A Property Market Update from Alexanders Removals & Storage

On reading the latest mortgage headlines it might be easy to conclude, with weary certainty, that things are about to get worse. With the current geopolitical tensions in the Middle East pushing oil prices higher and some high-street lenders announcing rate increases, the outlook seems gloomy at first glance. But it is worth pausing because the underlying direction of travel for borrowers remains firmly positive. The story is, in fact, far more encouraging, and the numbers prove it.

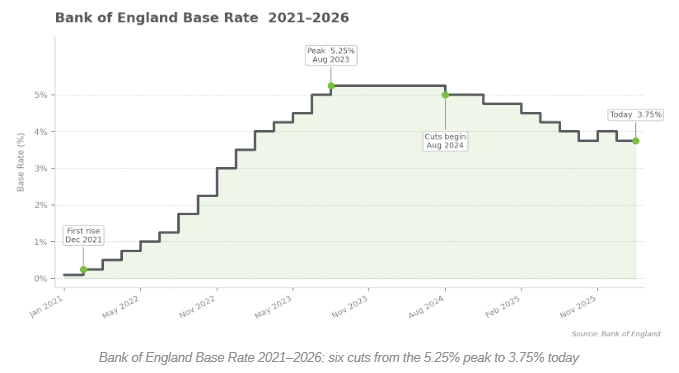

The bigger picture, one that tends to get crowded out by the noise of daily market movements, is this: Britain’s mortgage market has quietly undergone one of its most dramatic improvements in a generation. Since the Bank of England began cutting its base rate in August 2024, borrowers have watched that headline rate fall six times, from its peak of 5.25% all the way down to the current 3.75%. The great monetary tightening cycle, which turned the dreams of millions of aspiring homeowners into a prolonged nightmare, is firmly in retreat.

Where We Actually Stand

To understand why optimism is justified, it helps to look at where mortgage rates stood just over a year ago and where they stand today. For a typical first-time buyer taking out a two-year fixed deal with a ten per cent deposit, rates have fallen from around 5.35% at the start of 2025 to approximately 4.49% by the year’s end. The effective rate on all new mortgages dropped to 4.09% in January 2026, according to Bank of England data — a meaningful reduction that has translated directly into lower monthly payments for hundreds of thousands of households.

Lenders have not merely been cutting headline rates, either. The choice of mortgage products has risen to its highest level in eighteen years. The number of 95% loan-to-value deals (the lifeblood of first-time buyers who can only muster a 5% deposit) is at its highest since March 2008. There are now more than 7,500 products available in the higher loan-to-value market, over a thousand more than a year ago. For those who have spent years feeling locked out of homeownership, this expansion of options is genuinely significant.

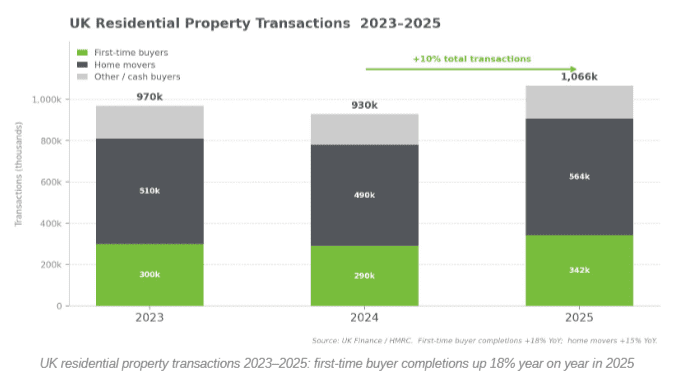

The housing market itself has responded. Total residential transactions in 2025 were ten per cent higher than in 2024. First-time buyer mortgage completions rose eighteen per cent year on year. Home mover activity climbed fifteen per cent. These are not the statistics of a market in crisis; they are the statistics of a market finding its feet after a prolonged and painful correction.

The Geopolitical Complication

All of which makes the recent events rather more frustrating than catastrophic. Renewed conflict in the Middle East has driven oil prices sharply higher, rattling global bond markets and pushing up the swap rates that lenders use to price fixed-rate mortgages. NatWest became the latest major high-street lender to announce repricing, following similar moves from several competitors. Markets have rapidly revised their expectations for Bank of England rate cuts: where City traders had previously anticipated multiple reductions through 2026, the consensus is now that the much-anticipated March 19th interest rate cut is “off the table.”

It would be dishonest to dismiss this as inconsequential. Swap rate movements do feed through into mortgage pricing, and a prolonged period of elevated energy costs could slow the Bank of England’s hand. Dutch bank Rabobank has gone so far as to suggest no further cuts at all in 2026, arguing that higher oil prices would feed quickly into domestic inflation.

Yet even the most cautious analysts are not forecasting a return to the grim peaks of 2023. Competition between lenders remains fierce, and that competitive pressure acts as a powerful brake on how far and how quickly rates can rise. The market dynamics have changed fundamentally: lenders are chasing volume, product ranges have been rebuilt from scratch, and the infrastructure of a more borrower-friendly era is already in place.

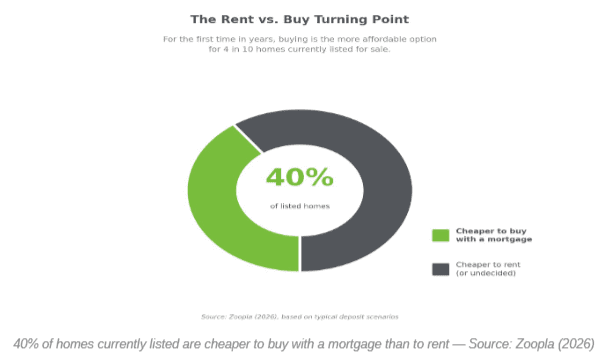

An estimated 40% of homes on the market are now cheaper to buy with a mortgage than to rent – a shift that is reshaping the calculus for millions of renters.

The First-Time Buyer Opportunity

Perhaps the most compelling reason for optimism lies with those who have longest felt excluded from the property market. Affordability has genuinely improved. According to Halifax, the house-price-to-income ratio reached its lowest level in over a decade in December 2025. Nationwide’s chief economist has noted that rising wages, combined with falling mortgage rates, have meaningfully eased the affordability squeeze that defined the 2022 to 2025 period.

Average UK house prices have risen a modest 0.3% in both January and February 2026, bringing the average property to £273,176. Annual growth stands at just one per cent. In a country which spent the better part of two decades fretting about runaway house price inflation, that kind of gentle, earnings-outpacing stability should be celebrated, not lamented.

For first-time buyers, an additional sweetener remains in place. The Freedom to Buy scheme – the successor to the Mortgage Guarantee Scheme – continues to support five per cent deposit purchases in 2026. Meanwhile, Zoopla data shows that the number of homes available for sale has risen six per cent compared with the same point last year, with February on course to record the highest number of new listings in a decade. More choice, at more sustainable prices, with better deposit support: the stars are aligning for first-time buyers in a way they have not done for years.

Property analysts at Zoopla have also noted a striking shift in the rent-versus-buy calculation: approximately 40% of homes currently on the market are now cheaper to purchase with a mortgage than to rent, assuming typical deposit scenarios. That figure would have been unthinkable at the height of the rate-rise cycle. It suggests that, for many renters still waiting on the sidelines, the financial case for buying has already been made, regardless of whether the Bank of England cuts rates or not.

What The Bank of England Is Telling Us

The February meeting of the Bank’s Monetary Policy Committee provided something that is all too rare in financial commentary: nuance. The committee held rates at 3.75% but four of its nine members voted for an immediate cut to 3.5%. The Bank itself signalled that inflation is now forecast to return to its two per cent target this spring, somewhat sooner than previously anticipated, and that scope remains for further cuts later in the year if the economy evolves as expected.

That is not the language of an institution bracing for another tightening cycle. It is the language of a committee that has done the hard work. Inflation has fallen from a peak of over ten per cent to three per cent, and is now carefully managing the final stage of the descent. The next MPC meeting falls on 19 March. Whatever the outcome, the medium-term direction of policy remains downward.

Long-range forecasts, which were pointing to a base rate of 3.25% by the end of 2026 before the latest geopolitical flare-up, have been revised upward, but not abandoned. The most bearish credible scenario sees the base rate ending the year where it started, at 3.75%. Undoubtably the era of five per cent-plus borrowing costs is over.

The Practical Advice

For borrowers approaching the end of a fixed-rate deal, the practical message from mortgage brokers is consistent: act rather than wait. Most lenders allow borrowers to secure a rate several months before completion, and many will switch to a lower product if pricing improves before the deal begins. Locking in a rate today does not mean forfeiting the chance to benefit from future cuts; it means protecting oneself against the possibility that they do not materialise, while retaining the optionality to switch downward.

For those on two-year fixes taken out in 2024, when rates had already begun to ease, the remortgaging arithmetic has improved markedly. For those rolling off five-year deals struck in the ultra-low-rate era before 2022, the adjustment will still sting, though nowhere near as sharply as it would have done two years ago.

For aspiring buyers still renting, the question is whether to wait for further rate cuts that may or may not materialise, or to take advantage of a market that already looks more affordable than at any point in recent memory, with broader product choice and genuine government support. History suggests that those who wait for perfect conditions in the property market tend to spend a very long time waiting.

If you’re ready to move, the next step is finding a removals company you can trust. Alexanders Removals & Storage has been helping Londoners move home since 2002, completing over 1,600 moves a year and rated 5-star Excellent on Trustpilot. Call us on 0333 800 2323 or book a free survey here.

Key Data at a Glance

- Bank of England Base Rate (March 2026): 3.75% Down from a peak of 5.25%

- Effective rate on new mortgages (January 2026): 4.09%

- UK house price annual growth (February 2026): 1.0% | Average price: £273,176

- Housing transactions in 2025: up 10% year on year

- First-time buyer completions in 2025: up 18% year on year

- Number of 95% LTV mortgage products: highest level since March 2008

- UK inflation (January 2026): 3.0% Bank of England target: 2%

- Next MPC meeting: 19 March 2026

Source: Bank of England, Nationwide Building Society, Halifax, UK Finance, Moneyfacts, Zoopla. This article is for informational purposes only and does not constitute financial advice. Mortgage products and rates are subject to change. Always seek independent financial advice before making borrowing decisions.